How can banks manage the escalating costs of fraud while maintaining regulatory compliance and customer trust in 2026? Learn how Al-driven intelligence layers are modernizing legacy detection systems, optimizing operational costs, and enabling financial institutions to deploy enterprise-grade fraud prevention frameworks in weeks.

For decades, the banking industry operated on a foundational philosophy of manual verification and physical oversight. Fraud prevention was synonymous with rigid checklists, face-to-face KYC protocols, and a heavy reliance on human intuition to flag suspicious activity. This system worked in an era of slower settlement cycles, but the rapid digitization of finance has introduced a critical conflict: the luxury of time has vanished. In an era of instant payment rails and global digital identities, the traditional manual process has become an operational bottleneck, creating friction that leads to lost capital and abandoned customer relationships.

Today, bank owners and Chief Risk Officers face a dual-front pressure. They must adhere to stringent regulatory mandates from bodies like the RBI, the SEC, or the EBA, while simultaneously defending against automated attacks that exploit the milliseconds between authorization and settlement. The challenge is not simply stopping a thief; it is maintaining a seamless, compliant operation in an environment where a legitimate user and a sophisticated script often exhibit similar behavioral patterns to a legacy system.

"Banks do not suffer from a lack of data, but from a lack of orchestrated intelligence that can turn disparate signals into a unified risk decision."

The Evolution of Risk: Why Manual Systems Failed

The transition from traditional banking to digital-first platforms was intended to increase efficiency, yet it inadvertently expanded the attack surface. Legacy systems, built on static "if-then" rules, were designed for a world where transactions took days to settle. In 2026, where settlement happens in milliseconds, these systems are structurally inadequate.

When a bank relies solely on manual intervention or basic rule-based triggers to meet regulatory standards like KYC, it often results in a false positive crisis. Genuine customers find their accounts frozen or transfers blocked because they deviate slightly from a hard-coded norm. This friction is a direct threat to the bank's business growth and capital efficiency.

What are different Fraud Types in Banking?

To understand how Al mitigates risk, we must first categorize the modern threats that bypass traditional manual perimeters. These are multi-stage identity and liquidity attacks that require sub-second detection.

Card and Payment Fraud

Card-not-present (CNP) fraud remains a dominant issue, but the emergence of real-time payment rails Like UPI or FedNow has changed the stakes. Because funds are settled instantly, there is no window for human review. If a fraud detection system is not autonomous and real-time, the capital is gone before an alert is even generated. According to Juniper Research, online payment fraud losses are projected to exceed $91 billion by 2028, largely driven by these high-speed transaction environments.

Account Takeover and New Device/Login Fraud

Account Takeover (ATO) represents a failure of traditional credential-based security. Once a criminal acquires legitimate usernames and passwords, the legacy system views them as the valid account holder. This is where the manual "checklist" fails: the credentials are correct, but the intent is criminal. Detection now requires a deeper layer of intelligence that monitors intent rather than just access.

How Al Is Used in Financial Fraud Detection

The solution is the implementation of an Al-driven Intelligence Layer. This layer does not replace the core banking system; instead, it acts as a high-speed security skin that orchestrates data in real-time to differentiate between a human user and an automated script.

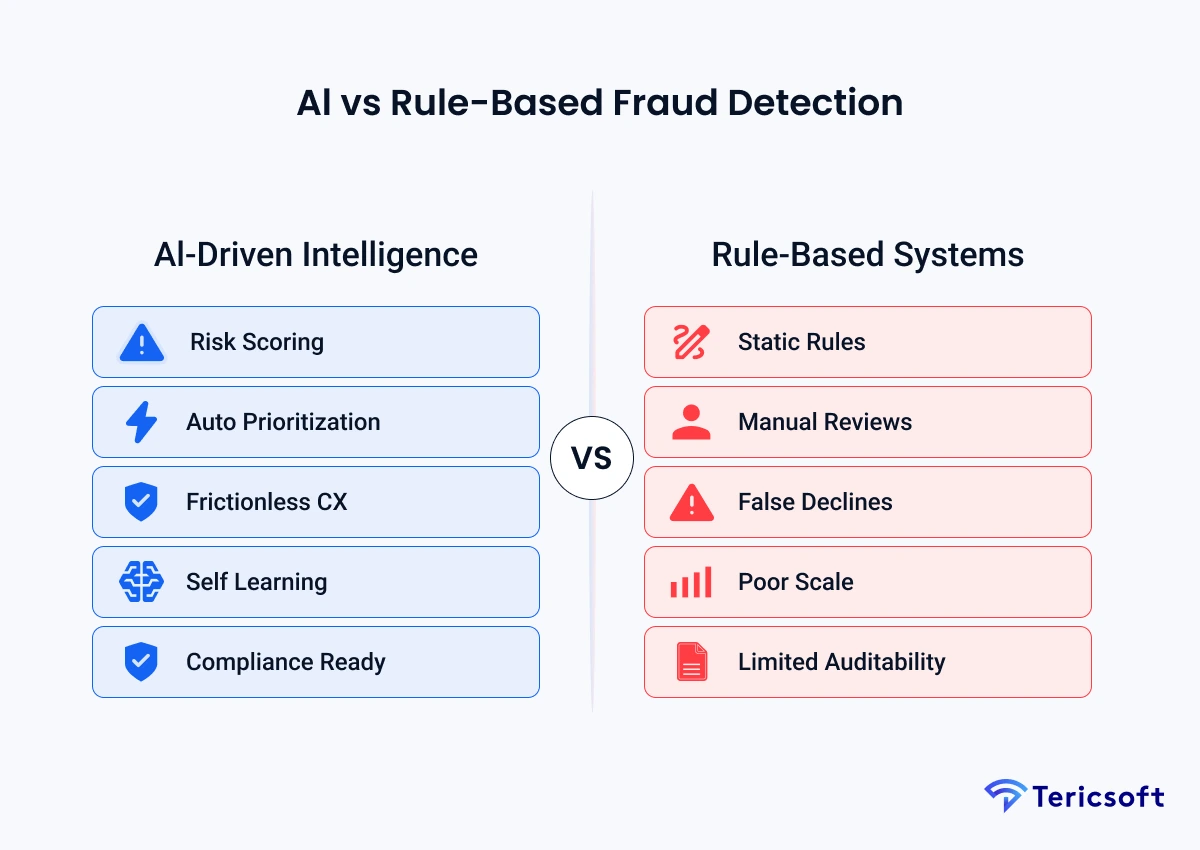

Al vs Rule-Based Fraud Detection

While rule-based systems catch basic, repetitive errors, they are static and easily bypassed by criminals who "fuzz" the rules. Al-driven intelligence utilizes probabilistic scoring to evaluate the risk of a transaction based on hundreds of variables simultaneously.

"Fraud doesn't follow rules anymore. So systems that rely only on rules will always be one step behind."

Data Banks Use to Detect Fraud and Prevent Financial Crime

To move away from the manual "one-size-fits-all" approach, Al intelligence layers must ingest and orchestrate data that goes beyond basic transactional parameters. This data is categorized into three critical signal environments:

- Transactional and Contextual Metadata: This involves looking past the "amount" of a payment to analyze the underlying lifecycle of the request. It tracks gateway latencies, the specific API calls made during the session, and the settlement path chosen. If a transaction follows a path that is technically uncharacteristic for a bank's standard infrastructure, it is flagged as a potential injection attack.

- Dynamic Behavioral Biometrics: This is the analysis of the human-to-device interaction layer. Unlike static KYC, which is a one-time check, behavioral biometrics is a continuous process. It monitors keystroke dynamics, the specific angle at which a mobile device is held, and the navigational flow through the application. These micro-behaviors are nearly impossible for automated scripts or remote-access trojans (RATs) to replicate perfectly.

- Environmental and Hardware Intelligence: This layer evaluates the integrity of the user's digital environment. It checks for device "health" indicators, such as the presence of emulator software, jailbreak or rooting attempts, and the use of sophisticated VPNs or proxy servers designed to hide geographic origins. By correlating this hardware data with the user's historical profile, the system can detect high-risk logins even if the credentials provided are 100% accurate.

Different Techniques Banks Use for Al Fraud Detection

Modern fraud prevention requires a sophisticated architectural approach that can process millions of events per second.

Anomaly Detection and Behavioral Analytics

This technique establishes a digital baseline for every customer. By observing months of legitimate behavior, the Al learns what a normal interaction looks like for a specific user. When a transaction falls outside of this statistical norm, the system assigns a risk score. According to the Association of Certified Fraud Examiners (ACFE), proactive Al-driven analytics help organizations detect fraud 50 percent faster, which is critical for preserving institutional capital.

Real-Time Signal Orchestration

Real-time detection requires a system that can ingest signals from disparate sources, such as IP reputation databases and device fingerprints, while a transaction is still pending. Tericsoft specializes in building these high-speed orchestration systems, allowing banks to make a definitive risk decision in under 30 milliseconds. By moving the intelligence to the edge of the banking network, fraud is stopped at the gate before it touches the core ledger.

Graph Analytics for Network Link Analysis

Fraudulent activity rarely happens in isolation. Sophisticated criminals use networks of accounts to move money quickly through a series of small, rapid transfers. Graph analytics allows banks to visualize these connections in real-time. If multiple accounts are opened using similar device footprints and all funnel money to a single entity, the graph model flags the entire network as a high-risk cluster.

Why Explainable Al Matters for Fraud Decisions

In the financial industry, using Al introduces a new risk: the "Black Box" problem. Regulators demand to know why a transaction was blocked. If a bank cannot explain its automated decisions, it faces severe compliance penalties.

Explainable AI (XAI) provides a transparent reasoning layer. It produces an audit-ready log for every decision, such as: "Transaction blocked due to unusual geographic origin combined with an uncharacteristic navigation path for this user." This transparency ensures the bank remains compliant while benefiting from Al's speed.

"In banking, accuracy without explainability is a liability."

Challenges in Al Fraud Detection in Banking

Modernization is a strategic necessity, but it requires overcoming several operational and technical hurdles that can impact a bank's bottom line and reputation.

Challenge 1: High False Positives and Customer Churn

Legacy systems often utilize broad, rigid parameters that fail to account for the nuances of modern life, such as a customer shopping while on vacation. This results in a high volume of false positives, where legitimate transactions are blocked. For a bank, this creates a "customer friction" crisis that leads to transaction abandonment and high churn rates. Furthermore, it creates "alert fatigue" for fraud teams, where analysts are buried under a mountain of irrelevant warnings, increasing the risk that a genuine threat will be ignored.

The Solution: Use behavioral analytics to refine risk scores by creating a unique, contextual baseline for every customer. By understanding individual intent rather than just checking against a static rule, banks can ensure only high-risk activity requires human intervention.

Challenge 2: Model Bias and Contextual Data Decay

Al models are only as effective as the data they consume. If a model is trained on historical data that is incomplete or lacks diversity, it can develop biases, unfairly flagging specific user groups or geographic regions. Additionally, as fraud tactics evolve, older models suffer from "data decay," where their logic becomes obsolete against new, sophisticated attack patterns.

The Solution: Implement a continuous learning loop where human fraud analysts provide feedback on model outputs. This "human-in-the-loop" approach ensures that models are retrained using diverse, real-world outcomes and synthetic data that simulates emerging fraud trends.

Challenge 3: Regulatory Compliance and The Black Box Liability

Global regulators, including the RBI and the SEC, demand that banks maintain full control and accountability over their automated processes. A "black box" model that cannot justify its decisions is a massive compliance liability. If a bank cannot produce an audit trail explaining why a specific corporate transfer was frozen, it faces severe legal repercussions and a loss of institutional trust.

The Solution: Deploy explainable Al (XAI) frameworks that provide a clear, defensible reasoning layer for every transaction. This ensures that every automated decision is transparent, justifiable, and fully aligned with global regulatory mandates.

Benefits of Al Fraud Detection for Banks

The shift to an Al-led intelligence architecture provides a clear competitive advantage:

- Capital Preservation: Reducing successful fraud and subsequent capital flight.

- Operational Savings: Minimizing the need for massive manual review teams through automated prioritization.

- Customer Loyalty: Providing a seamless experience for legitimate users.

- Regulatory Compliance: Ensuring all decisions are transparent, auditable, and defensible.

Future of Al Fraud Detection in Banking

The future of financial security is moving toward Predictive Prevention. We are moving toward a world where Al predicts which accounts are likely to be targeted based on global threat intelligence before an attack even begins.

"The future of fraud detection is not catching fraud faster, but preventing it before it happens."

How Tericsoft Helps Banks Implement Al Fraud Detection

Tericsoft specializes in building the Al Intelligence Layer, a high-performance architecture that integrates with your current infrastructure to provide real-time risk orchestration. We understand that banks cannot simply turn off their legacy systems, so we build the security layer that modernizes them from the outside in.

We help banking leaders:

- Orchestrate Signal Intelligence: We connect disparate data silos into a single, real-time risk engine.

- Build Real-Time Systems: Our team develops the high-speed infrastructure required to stop fraud on instant payment rails.

- Ensure Regulatory Transparency: We implement XAI frameworks that keep you ahead of compliance requirements without sacrificing speed.

Still relying on rule-based fraud systems? Let AI stop fraud before it impacts your customers.

AI fraud detection in banking uses real-time analytics and machine learning to identify suspicious transactions and prevent financial fraud.

AI analyzes transaction behavior, device signals, and contextual data instantly to flag high-risk activity before settlement occurs.

Explainable AI helps banks justify automated fraud decisions, ensuring transparency, auditability, and regulatory compliance.

AI adapts to new fraud patterns and reduces false positives, while rule-based systems rely on static thresholds and manual reviews.

Yes, when built with explainable AI and audit trails, AI fraud detection meets regulatory requirements and compliance standards.