Can banking leaders truly eliminate compliance fatigue, or are we simply digitizing regulatory friction? The answer lies in moving beyond manual oversight toward intelligent systems that prioritize risk detection over data volume.

In the quiet hours of a typical Tuesday, a mid-sized global bank processes roughly four million transactions. Behind the scenes, a legacy rules-based system, built on logic defined five years ago, triggers 45,000 alerts. By Wednesday morning, a team of two hundred compliance officers will begin the grueling task of manually reviewing these flags. Statistically, 95% of these alerts will be "false positives," noise generated by a system that understands rules but fails to comprehend context. This is the "compliance tax" of the digital age.

For decades, banking compliance was a defensive moat, a necessary but static wall of manual checks and binary logic. However, as the global volume of digital payments is projected to reach $70 trillion by 2029, the wall is cracking. Financial institutions are moving beyond manual oversight toward the next evolution: AI in Banking Compliance. This shift represents a transition from reactive "box-ticking" to intelligent, predictive, and automated regulatory monitoring.

Why Compliance Has Become One of the Biggest Challenges for Modern Banks

The financial ecosystem has transformed into a high-velocity, borderless network. For modern banks, the challenge is no longer just "following the rules"; it is managing the sheer scale of data that those rules now apply to.

Increasing Regulatory Pressure Across Global Financial Systems

Regulatory bodies such as the FCA, FinCEN, and the European Banking Authority are no longer just looking for compliance; they are demanding operational resilience. According to the LexisNexis True Cost of Financial Crime Compliance Study, compliance costs increased for 98% of financial institutions in 2023, with total global spending on financial crime compliance now exceeding $200 billion annually.

The Growing Complexity of AML, KYC, and Risk Monitoring

Banks today must navigate a labyrinth of Anti-Money Laundering (AML) laws, Know Your Customer (KYC) mandates, and evolving sanctions lists. The complexity is compounded by "regulatory discord," where rules in the UK might differ slightly from the US or EU, forcing global banks to maintain fragmented, localized compliance engines that rarely communicate with one another.

Why Traditional Compliance Systems Struggle to Keep Up

The failure of traditional systems lies in their rigidity. Rule-based engines operate on "if-then" logic. If a transaction exceeds $10,000, flag it. This approach is easily bypassed by sophisticated criminals who use "smurfing," which involves breaking large sums into small, unregulated amounts, or complex corporate shells.

“As financial transactions grow in volume and complexity, traditional rule-based monitoring systems often fall short in detecting sophisticated fraudulent activities.”

— Enterprise Financial Services Research Team, Tookitaki (RegTech Platform)

Furthermore, as digital banking grows, the manual review of these alerts becomes physically impossible to scale without ballooning headcount costs.

Strategic Insight: From Cost Center to Competitive Differentiator

A critical shift in the thought-leadership landscape is the realization that AI-driven compliance is no longer just an operational expense. Forward-thinking institutions are viewing advanced regulatory monitoring as a strategic asset.

By reducing friction in the onboarding process and minimizing the "false positive" rate for legitimate customers, banks can significantly improve the user experience. In a market where digital agility is a primary factor in customer retention, a "low-friction" compliance experience becomes a powerful competitive differentiator.

What Is AI in Banking Compliance?

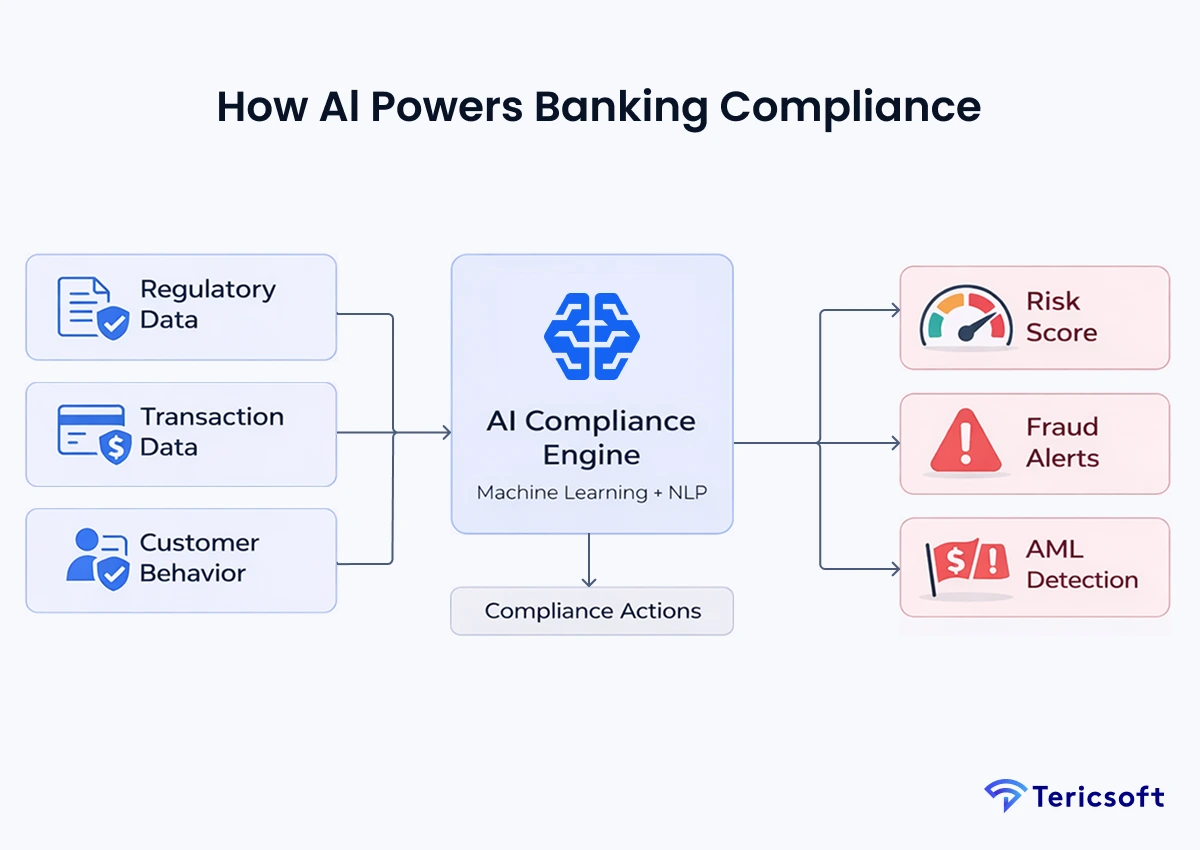

AI in Banking Compliance is the application of machine learning (ML), natural language processing (NLP), and deep learning to automate and enhance the regulatory oversight of financial activities. It is the brain that sits on top of the banking infrastructure, analyzing signals that are invisible to the human eye.

Defining AI-Powered Regulatory Compliance

Unlike traditional software, AI-powered compliance systems do not wait for a rule to be broken. Instead, they learn the "baseline" of normal behavior for every customer and entity. When a transaction deviates from that baseline, even if it technically falls within the legal limits, the AI identifies it as a risk.

How AI Systems Interpret Financial Data and Regulatory Signals

Modern AI platforms utilize Natural Language Processing to read and interpret thousands of pages of new regulatory documentation published every year. By converting "legal-speak" into digital logic, AI helps banks update their monitoring parameters in real time, ensuring they are never behind the latest legislative curve.

The Role of Machine Learning and NLP in Compliance Monitoring

- Machine Learning: Analyzes historical transaction data to identify hidden patterns of financial crime.

- NLP: Scans news, sanctions lists, and even internal emails to identify Adverse Media or internal conduct risks that could lead to regulatory fines.

Core Compliance Functions Where AI Is Transforming Banking Operations

The integration of artificial intelligence into core banking workflows allows for a granular level of scrutiny that was previously impossible. By embedding AI into the primary pillars of regulatory oversight, institutions can move from defensive posturing to proactive risk management.

AI for Anti-Money Laundering (AML) Detection

Modern money laundering techniques have evolved into multi-layered schemes designed to bypass threshold-based detection.

The Challenge: Traditional AML systems generate a mountain of noise, making it difficult to find the actual instances of money laundering. Rule-based systems often miss complex patterns like "structuring" or circular transfers that take place across multiple jurisdictions.

The AI Solution: AI employs Graph Theory and Link Analysis to visualize connections between seemingly unrelated accounts. It identifies mule networks and circular payment patterns that manual investigators would take weeks to map. Furthermore, machine learning models can detect "nested" corporate structures and high-frequency, low-value transfers that signal illicit layering activities.

AI in Know Your Customer (KYC) and Identity Verification

The first line of defense in banking is knowing exactly who is entering the financial system, yet this remains a significant friction point for legitimate users.

The Challenge: Manual KYC onboarding can take 15 to 30 days, leading to high customer drop-off rates and excessive operational overhead. Human review is also susceptible to sophisticated identity theft and document forgery.

The AI Solution: AI automates document verification using computer vision to spot tampered IDs and uses biometric liveness checks to prevent deepfake fraud. This reduces onboarding time to minutes while increasing the security of the identity claim. Beyond initial entry, AI systems continuously refresh customer risk profiles by analyzing behavioral signals.

AI for Transaction Monitoring and Fraud Detection

The velocity of digital payments requires a monitoring system that can decide the legitimacy of a transaction in the time it takes to authorize a card swipe.

The Challenge: Fraudsters adapt faster than rules can be written, often exploiting the latency between a transaction and its subsequent manual review.

The AI Solution: Modern architectures for AI-driven fraud detection in banking utilize adaptive risk scoring to assign a score in milliseconds based on location, device, and historical behavior. High-risk transactions can be automatically frozen or sent for immediate high-priority review. By utilizing unsupervised learning, these systems can even identify "zero-day" fraud types that have never been seen before by recognizing anomalies in data distributions.

AI for Regulatory Reporting and Audit Automation

Reporting is perhaps the most critical yet least innovative aspect of traditional compliance, often relying on spreadsheets and manual data aggregation.

The Challenge: Preparing reports for regulators is a labor-intensive process prone to human error, often leading to incomplete filings that invite regulatory scrutiny.

The AI Solution: AI automates data extraction from disparate banking systems and populates regulatory filings with 99% accuracy. These systems can automatically flag missing data points and suggest corrections before the report is submitted, significantly reducing the likelihood of "failure to report" penalties.

Strategic Insight: The Emergence of Agentic AI in Compliance

A significant evolution in the field is the shift from static automation to "Agentic" AI workflows. Unlike earlier generations of AI that merely followed a single model output, Agentic AI systems can break down a complex regulatory query into sub-tasks.

For example, an AI agent could simultaneously scan a global sanctions list, cross-reference it with a customer's recent behavioral shift, and query an internal ledger to assess risk. This multi-step reasoning allows the AI to act more like a "digital investigator," synthesizing multiple data points into a cohesive risk narrative before presenting it to a human officer.

AI-Driven Regulatory Intelligence: Mastering the Change

Financial institutions are currently overwhelmed by the sheer volume of "regulatory change." On average, a major global bank must track over 200 regulatory updates per day across various jurisdictions.

AI for Regulatory Change Management

AI-driven intelligence platforms can automatically scan, categorize, and prioritize these updates. By mapping a new regulatory circular to the specific business units it affects, AI ensures that no legislative shift goes unnoticed. This reduces the "compliance lag" that often leads to accidental non-compliance.

Automated Interpretation of Regulatory Circulars

Using Large Language Models, these systems can "read" new circulars and summarize their impact on current internal policies. Instead of waiting for a legal team to digest a 500-page document, the AI can provide an instant delta analysis, highlighting exactly where existing workflows need adjustment.

Simulating Regulatory Impact

Advanced AI models can now run simulations to see how a proposed regulatory change might affect the bank’s risk profile or profitability. By creating a "Digital Twin" of the bank's compliance framework, leaders can stress-test their operations against hypothetical future regulations, moving from reaction to strategic preparation.

Overcoming the Historical Hesitation: Security, Privacy, and Trust

For years, the banking industry stood on the sidelines of the AI revolution. The hesitation was rooted in a valid fear: "If we put our data into an AI, do we lose control of it?"

Early AI models required data to be sent to third-party clouds, which was a non-starter for institutions handling sensitive PII. Furthermore, "black box" algorithms, where the AI makes a decision but cannot explain why, created a regulatory nightmare.

The Modern Solution: Private LLMs and Secure AI Layers

Today, the paradigm has shifted. Banks no longer need to choose between innovation and security.

- On-Premises & Private Cloud Deployment: Modern AI architectures allow banks to run Private Large Language Models (LLMs) within their own firewalls. Your data never leaves your environment.

- Explainable AI (XAI): We have moved beyond black box logic. Advanced AI platforms now provide reasoning paths, showing the exact data points and regulatory rules that led to a specific risk flag.

- Data Masking & Synthetic Data: AI can now be trained on synthetic versions of banking data that maintain statistical patterns without exposing actual customer identities.

Challenges and Risks: How to Implement Successfully

Successfully deploying AI in a highly regulated environment requires a strategic approach that goes beyond technical integration. It involves navigating the intersection of data integrity, regulatory expectations, and institutional governance.

The Data Sovereignty Paradox

A unique challenge for global banks is navigating "Data Sovereignty," where different jurisdictions have conflicting rules about where data can be stored and processed. Global institutions often struggle with localized mandates such as GDPR or India's DPDP Act, which restrict the movement of sensitive financial data across borders.

AI systems must now be designed with "localized intelligence" layers. These layers can process data within a specific region to comply with local laws, while still allowing the global institution to gain centralized risk insights. This requires a sophisticated architecture that balances local privacy with global oversight.

Data Quality and Fragmented Financial Systems

The Risk: AI is only as good as the data it consumes. Fragmented data silos, often a result of legacy mergers and acquisitions, lead to incomplete risk profiles and inaccurate model outputs.

The Fix: Build a Unified Compliance Data Architecture. Consolidate transaction logs and customer metadata into a single Source of Truth. Banks should prioritize data cleansing to ensure that AI models have access to high-quality, normalized datasets.

Model Transparency and Regulatory Concerns

The Risk: Regulators will reject AI decisions that cannot be defended in an audit. If a bank cannot explain why a customer was flagged as high-risk, it faces significant legal exposure.

The Fix: Maintain human-in-the-loop governance. AI should act as a high-powered filter that empowers human compliance experts. Establishing a dedicated Model Risk Management (MRM) team to perform regular bias audits and performance drift monitoring is essential for long-term regulatory approval.

“Artificial intelligence enables financial institutions to detect suspicious activity faster, reduce false positives, and strengthen compliance outcomes.”

— Neotas Financial Crime Technology Team

The Future of AI in Banking Compliance

We are moving toward a world of Autonomous Compliance Monitoring. In this future, AI systems will not only detect risk but will automatically suggest remediation steps, draft regulatory filings, and even simulate what-if scenarios to test how a bank’s portfolio would react to new global sanctions.

The shift toward Continuous Compliance in real-time financial ecosystems will become the industry standard. Banks that fail to adopt these intelligent systems will find themselves unable to compete with the speed of digital-first fintechs and increasingly vulnerable to sophisticated financial crime.

Operationalizing AI-Driven Compliance Architectures

Enterprise AI platforms such as Tericsoft enable financial institutions to operationalize AI-driven compliance architectures without replacing existing banking infrastructure. By providing the secure, scalable layers required to connect banking data with regulatory logic, these platforms ensure that compliance is a core feature of every transaction.

Modern AI intelligence platforms enable CCOs and CIOs to detect complex risk patterns while maintaining absolute regulatory transparency. These solutions bridge the gap between legacy core banking and the demands of a real-time, global regulatory environment, allowing organizations to deploy AI-driven systems that align with enterprise governance standards.

About Tericsoft

Tericsoft is an enterprise AI transformation partner helping financial institutions modernize risk, compliance, and regulatory monitoring systems. We build secure, scalable AI architectures, including Private LLM deployments, that integrate directly with existing banking infrastructure. Our intelligence platforms enable CCOs and CIOs to detect complex risk patterns, reduce operational friction, and maintain absolute regulatory transparency.

We help organizations deploy AI-driven systems that align with global financial regulations and enterprise governance standards, ensuring that innovation never comes at the cost of security or compliance integrity.

AI in banking compliance refers to the use of machine learning, natural language processing, and data analytics to automate regulatory monitoring, detect suspicious financial activity, and improve risk management across banking operations.

AI systems analyze large volumes of transactions in real time, detect behavioral anomalies, and reduce false positives in alerts. This helps compliance teams identify potential risks faster and respond more effectively to regulatory requirements.

Yes. AI models learn normal transaction behavior and detect unusual patterns instead of relying only on static rules. This significantly reduces false alerts and helps investigators focus on genuine financial crime risks.

AI automates document verification, biometric checks, and customer risk profiling. It can analyze identity documents, detect fraud attempts, and continuously monitor customer activity to maintain accurate compliance records.

AI improves risk detection accuracy, automates regulatory reporting, reduces operational costs, and enables real-time monitoring of financial activity, helping banks stay compliant in complex regulatory environments.